Savings Monthly Interest Calculator

- Monthly savings interest rate calculator

- Savings monthly interest calculator financial aid

- Savings monthly compound interest calculator

- Compound interest calculator monthly savings

- Monthly Savings Calculator | moneyfacts.co.uk

How does this monthly savings calculator work? Since one of the most preferred methods to save is to deposit an initial amount and then add monthly contributions to it within the limits you can afford, this personal finance tool aims to help you calculate the growth of your investment account in which you place regular savings at the beginning of each month.

Monthly savings interest rate calculator

For instance you set up your savings goal and a month later you lose your job? Will you still be able to keep your savings plan? Most probably not! That is why you should always keep an eye on few things such as: Protect as much as you can the income sources that are stable and take advantage of the ones that may constitute occasional or extra income sources, BUT do not risk losing your stable sources for secondary sources you cannot be sure about. Assess in an objective way your capacity to save on a monthly basis otherwise your plans may prove unrealistic. Rather set up a longer term to achieve your goal than to set up a higher level of monthly savings because is it a safer approach. Take account of inflation rate that affects your savings as such you need to be aware for instance of the fact that the $100, 000 you want to achieve today will represent a significant smaller amount after a certain number of years. Take a pessimistic rather than optimistic average annual interest rate scenario; otherwise you risk making a calculation of your account growth that will then prove to be false.

Savings monthly interest calculator financial aid

Let's start with the interest rate it pays, since that's the main reason anyone opens a savings account. The CIT Savings Builder pays one of the highest interest rates of any bank, currently at up to 1. 45% APY. And you don't need a large amount of money to get that rate either. The rate applies to minimum balances greater than $25, 000. But there is a workaround – one that will allow depositors with even the smallest account balances to earn the top rate. Even if you don't have $25, 000, you can still earn 1. 45% APY simply by making monthly deposits of $100 or more. So, if you can direct deposit at least $100 into your CIT Savings Builder account each month, from payroll savings or auto-drafted from an external bank account, you can earn the top rate. That's the big advantage with this account. Most high yield savings accounts do require a large minimum balance. But with the CIT Savings Builder monthly deposit system, depositors at all levels can take advantage of some of the highest interest rates in the industry.

Savings monthly compound interest calculator

The screenshot below shows that my estimated savings balance after 30 years is about $134, 500. In the graph, the interest earned is the difference between the End Balance (blue line) and the Cumulative Interest (magenta line). The graph shows that until about 10 years, the majority of the balance is the cumulative amount I've invested rather than interest earned. But, by the end of the 30 years, my balance is almost twice what I put in. Related Resources 401k Savings Calculator by - Similar to the calculator above, but specifically for 401k calculations, where you have an employer match, increasing salary, etc. CAGR Formula - Explains how to calculate annual growth rate for an investment. Retirement Savings Calculator - - Similar to the simple savings calculator, but specifically related to retirement (graphed by age) and less flexibility in making deposits. Savings Bond Calculator at - Includes the effect of federal taxes. Savings Calculator at Time Value of Money at - Formulas for calculating future value of annuities.

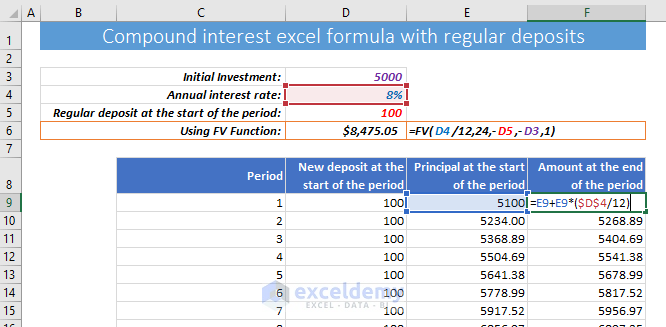

What is compound interest? The compound interest is the interest type in which the accumulated interest at a certain moment is added to the principal, such way that from the moment on, the return is calculated for both principal and the interest earned previously. Compared to the simple linear interest, the most important advantage it offers is that your money will increase at an exponential rate which translates into a more rapid growth of your account. The most used compounding types are monthly, quarterly, semiannually and annually. How is the compound interest with monthly contributions calculated? Let's take an example of an account with a starting principal of $100 with an annual return rate of 5% and a monthly addition of $10 for a year, applying the formulas presented above results the data: FV = will be final balance of your account at the end of the period. PV = $100 PMT = $10 i = 5% n = 12 Future Value = ( Capital Accumulation Formula) + ( Future Value of a Series) Future Value = ( ( (1 + i) n) * PV) + ( PMT * ( ( (1 + i) n+1 - (1+i)) / i)) Future Value = ( ( (1 + 0.

Compound interest calculator monthly savings

Got your savings goal set? Once you know how much you want to save each month, you will then need to find a savings account as a home for your money. An easy access account is usually the easiest place to start saving, with the least restrictions on how you can access your money. Our guide to managing your savings account will tell you more about the different accounts available and how often you can typically add or withdraw your money with each type of account. Savings guides Savings Guides What are challenger banks? A guide to what challenger banks are and their rise in popularity. How are my savings taxed? Every basic rate taxpayer in the UK currently has a Personal Savings Allowance (PSA) of £1, 000. 7 tips for saving for your first home Our top tips to help you save for your first home. How Moneyfacts works BALANCED. is entirely independent and authorised by the Financial Conduct Authority for mortgage, credit and insurance products. FREE. There is no cost to you. Our service is entirely free and you don't need to share any personal data to access our comparison tables.

Monthly Savings Calculator | moneyfacts.co.uk

This simple savings calculator can show you how to build your savings, or to reach any savings goal you have, just by inputting four pieces of information. How the Simple Savings Calculator works The savings account interest calculator uses two different methods – Monthly Deposit and Savings Goal. The Monthly Deposit method focuses on the outcome of making regular deposits. The Savings Goal sets your savings target, then helps you determine the monthly deposits you'll need to reach a specific savings goal. Either method can also serve to help you as a retirement savings calculator, as well since at least some of your retirement savings should be held in interest-bearing investments. Let's work examples using each of the two methods. The monthly deposit method Using the monthly deposit method, you'll need to enter four pieces of information: initial amount – this is your current savings balance. monthly deposit – enter how much you expect to deposit into savings each month. annual interest (compounded monthly) – enter the interest rate you expect to earn on your savings based on current rates.

- General liability insurance rates for subcontractors

- Savings account interest monthly calculator

- Bullet point list of Antonio Brown's achievements. Have at it Wes! : AroundTheNFL

- Music hosting sites.google.com

- Monthly Savings Calculator | moneyfacts.co.uk

- Calculate monthly interest calculator savings

- Satyam: A new system to redefine payroll that addresses complexities - The Economic Times